The President issued an executive order on August 8 to

provide for a payroll tax holiday in order to boost the economy during the current

pandemic. The holiday generally applies to employees earning less than

$100,000. The payroll tax holiday applies to only the 6.2% social security.

Medicare tax of 1.45% is not affected. This payroll tax holiday goes into

effect on September 1 (that’s Tuesday!!) However, the deferred social security

tax from September 1 through December 31 will need to be withheld between

January 1 and April 30 and repaid by April 30 next year, unless Congress votes

to forgive it all together. Here is my observation and why the executive order

is clear as mud!

First of all, the President exercised the disaster declaration authority under the Internal Revenue Code to accomplish the payroll tax holiday. The law allows the Treasury Secretary to defer the payment of payroll tax but not the waiver of the payroll tax. Therefore, employers still have the obligation to withhold the social security tax from employees unless Congress decides to eliminate the obligation from employers.

Let’s say an employer decides to follow the executive order and an employee leaves the company, it would be difficult for the employer to recoup the amount from the employee and it now becomes the employer’s burden to repay that employee’s portion of the social security tax by April 30.

In a different scenario, let’s say an employer decides not to follow the executive order and withholds social security tax from employees. Later on, if Congress decides to makes this a true payroll tax holiday, i.e. the employee’s portion of the social security is waived, the employer will need to return the withheld social security to the employees. In addition, since this amount now represents additional income to the employees, employers will need to report this additional income and withhold taxes on it. On the employee’s level, they will need to report it on their personal tax returns.

As you can see, each option carries its own risk. In the

end, the obligation of funding social security falls on employers. The Treasury

Secretary had said that he cannot force companies to follow the executive order

but he hopes many will participate. The US Chamber of Commerce has also said

that many businesses won’t implement the deferral because of the difficulties

in administering it and the greater burden for employers next year.

If you wish to discuss how best to proceed with regard to

your company, please Contact

Us.

We are living in unprecedented time. Life as we know it has

changed drastically, and so has your business. We know you have a lot of

questions and concerns about how to stay afloat, what does the short term cash

flows look like, how to navigate through the various government relief

programs, all while worrying if you can even afford getting sound advice right

now. Perhaps you see opportunities and want to collaborate with a trusted

partner. At CFO Connections, our business is built on relationships and on

helping you through the thick and thin of running your business. Here are ways

we are helping our community in this trying time:

On Thursday May 7 at 11am, we will host a complimentary “Ask Me Anything” zoom meeting with the owner and founder of CFO Connections Stella Valitutto, CPA. Stella is a CPA who has 20 years of experience serving businesses from start ups to growing to matured companies. You will have the opportunity to ask Stella those burning questions. Participants will be in a waiting area of the meeting and be admitted one by one. Please register to attend.

We are also offering a complimentary 30 minutes financial health assessment. We will provide you with actionable recommendations on how best to navigate through your business’s finances during this critical time. Contact us for a complimentary financial health assessment.

We are also offering deferred payments on our services in order to help businesses prioritize their cash flows. As you continue to run your business, the need for accurate and timely financial information is critical in making decisions, especially during this critical time. Contact us to discuss what works for you and your business.

We want to help as many business owners as we can so please

share with those you think could benefit from this event.

The government’s Paycheck Protection Program (PPP) from the

Coronavirus Aid, Relief, and Economic Security Act (CARES Act) provides much

needed relief to small businesses across the nation to keep workforce employed

and businesses afloat. You may have already applied for the loan and are

currently waiting for your bank to fund it. Now would be a good time to get up to

speed on the requirements of the program, the credits available to businesses,

some questions to ask your accountants, and our recommendations on how best to

handle the funds. We also have recommendations on ways to accelerate cash flows

from customers and defer payments to vendor during this crisis.

Paycheck Protection Program (PPP)

When the loan is funded, it is best to have the proceeds deposited

into a separate bank account so that disbursements from the proceeds can be

easily tracked and substantiated.

When figuring out the loan amount for the PPP loan, any

salary over $100,000 per employee is excluded. This is crucial because it

affects how much of the loan proceeds can be forgiven. For the highly

compensated employees (mainly the business owner and senior management), what

does this mean for their compensation?

The essence of the PPP is to keep workers employed so keep

an eye on your head count as it would have an impact on the amount of the loan that

can be forgiven.

How do you make sure that your PPP loan is forgiven? What

documentations is a business required to provide to substantiate the use of

proceeds?

The program provides for deferral of employer’s share of the

payroll taxes. If a business received a PPP loan and paid its employees with

the proceeds, when is it required to remit the employer’s share of the payroll

taxes? Have you reached out to your payroll processing company to understand whether

they have the capability to remit the correct amount of payroll taxes on your behalf?

The CARES Act also provides for an employee retention credit

at 50% of the first $10,000 wages per employee. Am I eligible to claim the

credit?

Can a business use tax-exempt income (e.g. forgivable PPP

loan) to generate deductions (e.g. payroll, mort int, rent, etc.)?

Cash Flows Management

Be proactive and contact your vendors. Those who were rigid

in their payment terms in the past may be accommodating due to current crisis. It

is important to maintain supplier relationships, avoid unnecessary turnover and

continue to meet customer demands.

Contact your customers to ask for payment even though most

businesses have been negatively impacted by this pandemic. Accept partial

payments and offer payment discount to entice customers to pay in full if they

have the ability.

Call credit card companies to inquire about delaying

payments and interest accrual. Most credit card companies are willing to make accommodating

during the current crisis.

Consider reducing discretionary expenses, such as certain

advertising and marketing expenses when your target customers are also

negatively impacted by this crisis, client meals/entertainment, etc.

Consider pay cut to ownership and senior management instead of reducing workforce so that you are able to meet customers’ demands when the turnaround occurs.

Having a trusted advisor on your side could mean keeping the train on the tracks and avoiding surprises. Contact us if you have questions on your mind.

We are living in unprecedented times right now. Many aspects of our lives are drastically changed, businesses are facing difficult decisions of preserving and prioritizing cash flows and maintaining a level of workforce to continue to meet customers demands. Therefore, having a good pulse on your cash flows requirement is extremely important, especially during the current crisis. Let’s take a look at what a cash flows projection entails and how it can help business owners see the reality and forge a logical path forward.

Traditional accrual basis income statement are often

unhelpful when it comes to cash flows management. It can especially be

misleading during a crisis. The concept of a cash flows projection is

relatively simple… tallying all your sources of cash and uses of cash during

the period of the analysis. The nuances of how to build a cash flows projection

is more complicated. It requires looking at your customers and suppliers and

your relationships with them. A well crafted cash flows projection will provide

a road map for running business while it becomes a critical tool in managing

cash flows during unprecedented times like this.

At the beginning of the projection, business owner will need

to consider making certain assumptions. For example, when will we receive

payments from our larger customers? What payment terms do we have with our

essential vendors? Will our relationships with our customers and vendors allow

us to accelerate receipts and defer payments in difficult times, such as the

current COVID-19 pandemic? Answering these questions will have a drastic impact

on the timing of the cash flows.

During the current COVID-19 crisis, business owner should also

consider whether there is any government stimulus financial assistance

available that should be factored into the cash flows projection. On the other

hand, any restricted use of the assistance should also be included in the projection.

If the financial assistance is in the form of a loan, business owner should

also consider the timing of the principle and interest payments in the projection.

In addition, small and medium size businesses has been

depending on using credit cards to pay certain expenses in order to defer cash

flows. This practice will have an impact on cash outflows and should be considered

when crafting a cash flows projection.

A cash flows projection is a tool that sets the foundation

and the basis for reviewing the assumptions made. Business owner should use

this tool to compare to actual results and determines whether the assumptions

are realistic. Are we being too conservative on projecting cash outflows but

too liberal on estimating cash inflows? If we identify gaps in cash flows, business

owner should begin exploring options for alternative source of capital. Perhaps

a discussion with its banking partner to review available options.

A cash flows projection and its assumptions should be

reviewed and updated on a weekly basis. When adjustment to the projection and its

assumptions is necessary, it is imperative to make those adjustments on a going

forward basis so that the going-forward projection is not skewed by timing

differences. Monitoring the projection on a weekly basis will give business

owner the opportunity to correct course timely when traditional accrual basis

financial statements will not. It allows business owner to see whether the

company will survive in the immediate and long-term. It is an immensely valuable

tool for business owner during ordinary time, and especially in distressed

situation.

If you want to know the survivability of your business, please contact us for a complimentary consultation.

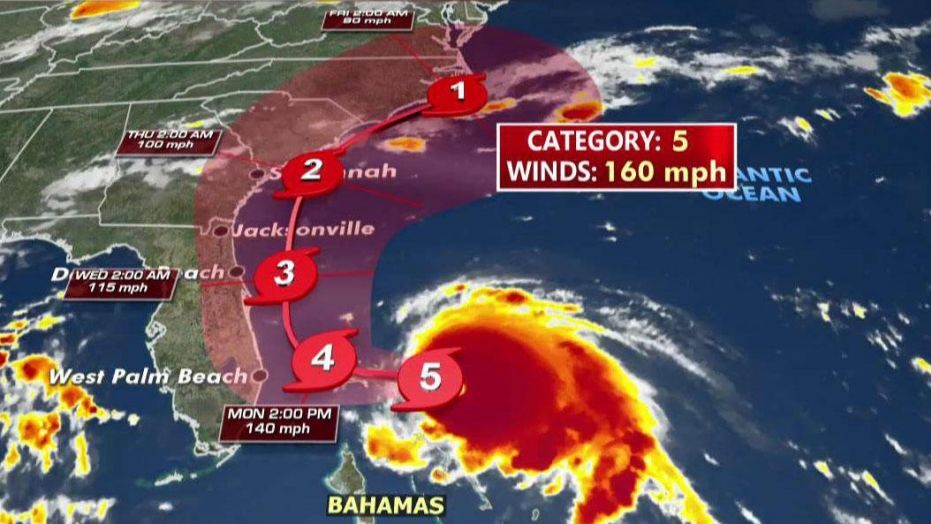

Hurricane Dorian was the most powerful tropical cyclone on record to strike the Bahamas, and is regarded as the worst natural disaster

in the country’s history. It was the fourth named storm, second hurricane, and the first major hurricane of the 2019 Atlantic hurricane season. Damage in the

Bahamas was catastrophic due to the prolonged and intense storm conditions,

including heavy rainfall, high winds and storm surge. Dorian is by far the costliest disaster

in Bahamian history, estimated to have left behind an exceptional

$7 billion in property damage. Hurricane Dorian then skirted up the Southeastern

United States and eventually made landfall in Cape Hatteras, North Carolina.

Insured losses from

Hurricane Dorian to the US will be between $500 million and $1.5 billion,

according to estimates by risk-modeling and analytics. The estimate

reflects property damage and business interruption to residential, commercial,

industrial and automobile lines of business. Companies that have

operations, significant customers, vendors, and employees in the Caribbean or

the Southeastern United States could have their operations significantly

interrupted and may have additional accounting considerations as a result of

the disaster.

Here are some of the accounting and financial reporting implications of these events.

Financial Statement Reporting and Disclosure Considerations

Companies that incurred losses may need to expand its footnote disclosure to discuss circumstances surrounding the losses, any insurance claims made and any expected insurance reimbursements. Any uncertainties related to the claims should also be disclosed. These considerations are especially important for publicly traded companies since the SEC has in the past asked registrants to expand disclosure to discuss the effect of natural disasters on their operations quantitatively and qualitatively, such as loss of a major supplier or customer.

Assets Impairment Considerations

Were assets damaged or destroyed as a result of the hurricanes? The most commonly affected assets after a natural disaster are fixed assets, inventories and accounts receivable. Writing off these assets may be necessary if they are destroyed.

How about the projected cash flows from certain assets? Are they negatively affected? Companies should consider writing down assets that were damaged and revisit their estimated useful lives.

Loans and Banking Considerations

Financial institutions, especially those that have a substantial amount of loans in the affected areas, should consider the need to increase their allowance for loan losses. In the immediate aftermath of Hurricanes Harvey and Irma, a number of financial institutions waived late fees and extended payment deadlines to their customers. Therefore, special considerations should be given to disclosing loss of revenues.

On the other hand, companies may need additional financing or amend the terms of their existing credit agreements with banks to increase its borrowing capacity. Companies should evaluate whether the amendments represent modification of existing debts, or extinguishment of the existing debts and commencement of new arrangements.

As a result of the negative impact the hurricanes had on companies’ operations, companies may be in violation of their loan covenants – assets as collaterals destroyed or financial covenants not in compliance. This may trigger default and affect the classification of the debt on the balance sheet.

Accounts Receivable and Revenue Recognition

Companies that do businesses with those in the affected areas should consider collectability, write offs or reserve against the receivables. Companies that allow extended payment terms to the affected businesses should consider its effect on revenue recognition (Topic 606) since revenue can only be recognized when collection is probable.

Idle Capacity

Companies may experience below normal production level as a result of power interruption or fuel shortage. When assets are temporarily idle, depreciation should continue. On the contrary, depreciation should discontinue when assets are permanently unproductive.

Insurance

To properly manage the risk losses from natural disasters, companies have insurance policies to cover property, casualty and business interruption claims. When companies believe that reimbursement from insurance is probable, the companies should recognize a receivable for the amount expected to be recovered. However, the amount recorded cannot be greater than the recorded losses. If companies expect to be reimbursed for an amount greater than its recorded losses, the different should be treated as a gain contingency, i.e. recognized only when realized.

For companies that filed claims under their business interruption policies, they would also follow the accounting for gain contingency, i.e. recognized only when realized.

The classification of insurance proceeds in the income statement depends on the nature of the claims. Proceeds should be recorded in the income statement once the gain contingency is resolved. There are not guidance provided for many different types of claims and therefore judgement should be applied.

Insurance proceeds should be presented in the statement of cash flows based on the nature of the item insured. If the proceeds are for damaged fixed assets, it would be an investing cash flow. If the proceeds are for business interruption, it would be an operating cash flow.

Tax Considerations

Since profitability is negatively affected, companies should evaluate whether deferred tax assets are “more likely than not” that they would be realized and whether a valuation allowance is necessary.

Nearly 75% of entrepreneurs will exit their businesses in 10 years.

Small business owners dedicate most of their life to their business. In many ways, it’s like their baby. They put all their savings and energy into it for years on end so it can thrive and truly succeed. They experience their share of ups and downs, but press ahead because they believe in the business and want it to grow.

But what happens when it comes time to hand over their business and let someone else take care of what they built with their sweat and tears? Doing so means accepting that they no longer make key decisions for its future. So, while they are still in the driver seat, what are some of the key financial and non-financial challenges they should be thinking about and planning ahead for?

1.Wealth preservation – Because the business owner’s wealth is concentrated on one company, business owner needs to think about the lifestyle he desires to have after exit through preserving wealth. A business owner should run an analysis on cash flows needed after exit in order to maintain current lifestyle to determine the amount of proceeds to be received when the business is sold.

2. Tax mitigation – this should be part of a strategy in exit planning since it will have a big impact on the amount of proceeds ultimately enjoyed by the business owner. A business owner looking to sell their business should consult tax professionals when planning for exit to minimize tax impact and maximize after tax cash flows.

3. Asset protection – after the business is sold, a business owner is on the radar and more exposed to a lot of people and could lead to potential frivolous litigations. Business owners need to work with professionals who can help them protect the cash flows in order to preserve wealth after exit.

4. Wealth transfer – A business owner needs to think about how to ultimately get the proceeds to family. This will be part of the estate planning process that is crucial for same or next generation wealth transfer.

5. Charitable intent – Most business owners want to fill the void that is left behind after selling their businesses and they often turn to philanthropy effort to make a difference in their communities.

How soon should a business owner start preparing to sell his business?

1.Time frame for exit planning – if you ask M&A professionals and business brokers, they would tell you yesterday is the perfect timing! Business owners who are heavy on operating the business often complain that they have no time to plan. With the strong market that we have currently, business owners could expect to sell their business in six months if they are willing to move quickly and aggressively towards their end goals. However, for proper planning for the challenges lie ahead – like the ones described – the recommended time frame is two to three years prior to exit to allow sufficient time to get personal affairs and business planning in order. Business owners often underestimate the amount of details that potential buyers will want to look at. Therefore, properly planning for exit will allow a business owner to focus on preparing for the potential buyers’ request for information. If you fail to plan, that often means you plan to fail.

2. Maximizing value – CPAs should advice clients reading for a liquidity event to get their financial statements in tip top shape; perhaps there has been some personal expenses running through the business that can be cleaned up or avoided? clean financials; what should we do now to get financials in order to achieve max value; what expenses are driving in the business now that shouldn’t be driving right now if we are planning for exit; how close can we get to accrual/GAAP basis?;

Other nonfinancial concerns

1.Filling that void after the exit – having your own business is very consuming of your life and it becomes a big part of you and your life. After a business owner sells his business, there is often a void, and something needs to fill that void since the life purpose isn’t there anymore. Business owners need to think about what they would like to do when they are no longer working and find new purpose in life.

2. Coordinate (quarterback) the process – A good advisor should be gathering a team to help a business owner build an exit strategy, and coordinating everything from A to Z. A good quarterback does not have to be an expert on taxes, financial reporting, estate planning, and business planning, all at the same time. Rather, a good quarterback must be a great communicator and be able to understand the emotions a business owner is going through during the process, and to pull together a team of other experts who have the best interest of the business interest at heart. CPAs typically have a knack in understanding the capabilities of other professionals. They are typically conservative and level-headed, and often compliment the high energy of business owners.

Do you have an advisor you can count on when you are ready to move to the next stage of your life?

Happy New Year! Now that the ball has dropped and the celebrations are settled, it’s time to get started on your resolutions. Some people want to lose a few pounds and eat more healthy. Perhaps you want to spend more time with friends and family? If you are a business owner, do you have financial resolutions for your business? Much like personal resolutions, most people don’t stick to them and by February, they are back to their old habits when the fun and newness wear out. Here are our top 4 financial resolutions for growing your business in the new year.

Assess your current situation – this is a great yearly tradition to find out where your business is – and where you want to be. Ideally, businesses should take a look at where they’ve been in early January. How did it do compare to forecast? Every business should have a forecast because it gives us clues as to what worked and what didn’t. It also tells us where we made the most of our money. Doing this will allow businesses to set goals that they have the best chance to accomplish this year.

Look at last year’s spending – did your money go where you really wanted it to go? If it didn’t, it will if you spend it mindfully. That means making spending decisions in the context of your goals. If one of your top goals is to expand the commercial line of your business, do you need to spend more on marketing to that segment of your business? Does that mean spending less on residential marketing? Spending mindfully may require you to reprioritize spending and being more aware of patterns. This will help you make better spending decisions every year.

Forecast your cash flows – this is perhaps one of the most important things to have in order to run your business and stay ahead of the game. After assessing your current situation, looking at last year’s spending and setting goals for this year, do you have the cash flows you need in order to accomplish your goals? Forecasting your cash flows will help you see whether there are gaps in your cash flows or excess capacity. Having that knowledge is crucial because it helps you determine whether you need to supplement your organic cash flows with outside funding. The sooner you discover gaps in cash flows, the better negotiating power you will have with lenders. If you have excess cash flows, you may be able to take advantage of discounts, pay off debts or invest to earn some interests.

Talk to your CPA periodically – this is an important preventative financial maintenance you can do to ensure the financial health of your business. Don’t wait till there is an emergency to talk to your CPA. Much like going to the emergency room, it is often stressful and expensive when an emergency brings you to see the doctor. Financial emergencies (e.g. embezzlement, lack of accurate and timely financial information, unexpected cash flows shortfall, unexpectedly high tax bill, unprepared for a financial audit, etc.) put you and your business in a stressful and expensive situation. The key is to minimize stressing your businesses from these emergencies by focusing your effort throughout the year. Your CPA can also help you carry out these financial resolutions for your business and set you up for success for the year.

Like the old saying “To know where you are going, you have to know where you’ve been”. So, look back, assess, evaluate; then look forward, put a plan together, engage your CPA to help guide you along the way and you are already many steps ahead of your competitors. At CFO Connections, we pride ourselves on being the financial compass for businesses. We’ve transformed chaos into stability for many businesses in Tampa and beyond. We love sharing best practices with business owners. To help you kick start and stick to your new year financial resolutions, we offer a one-hour complimentary consultation. Please click here if you want to have a successful 2019!